The Architecture of a Real Strategy (4/8)

Turning hypotheses into rules, entries, exits, and capital at work.

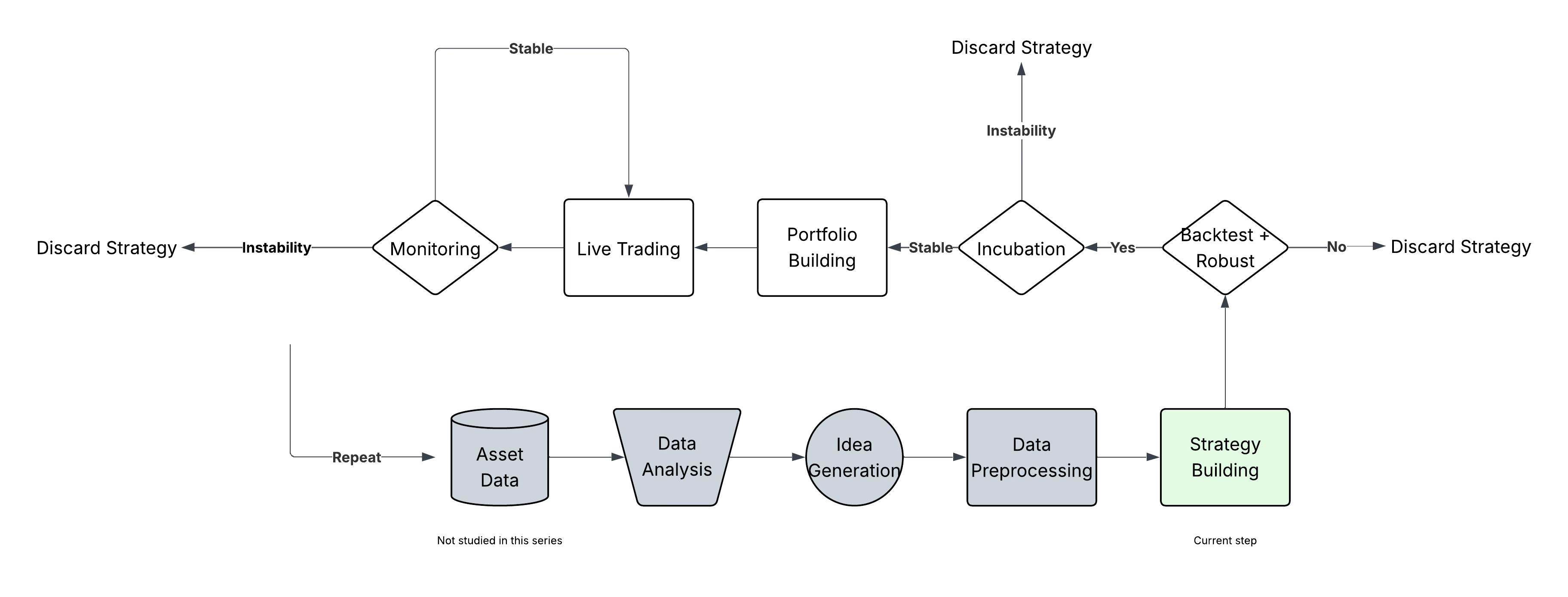

Now we get to the real construction phase.

The previous newsletters helped you define an idea and prepare your dataset. Now it’s time to turn that idea into a proper, structured strategy, something that can be tested, executed, monitored, and eventually traded.

This is the step where most people either overcomplicate or underthink. They pile up indicators or tweak random rules without understanding the big picture.

But a good strategy isn’t just about having a signal. It’s about knowing when to enter, when to exit, how much to trade, how to survive a bad streak.

In this newsletter, I’ll walk you through how I define these elements clearly and consistently. Not in vague terms, in blocks you can implement and stress-test later.

The next step will be about backtesting and robustness testing. But for now, let’s focus on building something worth testing.

1. Entry Logic: When and Why You Enter

This is where your strategy starts to take shape. You’re no longer just working with abstract ideas, you’re defining exactly what will trigger a position.

You need to be explicit here. Whether it’s:

A breakout above recent highs

A mean reversion signal after a sharp move

A model prediction suggesting high probability of a positive move

…it has to be something you can write in code and monitor live.

But raw signals aren’t enough. You also want to filter your entries:

Is the market liquid enough?

Is volatility too high (or too low)?

Is it during the right time window (avoid end-of-day noise, for example)?

Is the spread acceptable?

These filters are often more important than the signal itself. They define where your strategy is allowed to play, and that has a direct impact on performance stability.

If you're using machine learning, then you also need to convert the model's output into an actual entry trigger:

A classification model might output a probability (e.g. 0.87 chance of "up"), do you enter above 0.7? 0.8?

A regression model might give a forecasted return, do you enter if it’s above X basis points?

There’s no universal answer here. But you need to write it down clearly:

“I enter long when volatility is low, spread is below 1 pip, and the model’s output is above 0.8.”

My tip: The simpler and more explicit, the better.

2. Exit Logic: When and How You Close

Knowing when to get in is only half the work, knowing when to get out is just as crucial.

Your exit logic defines how you turn a signal into a profit (or a controlled loss). Without a clear plan, you end up second-guessing, chasing moves, or holding on too long.

There are three big families of exits:

Profit targets: You take the gain when the price hits a predefined level, for example, +2% return or a certain multiple of ATR.

Stop losses: You cut the trade if it goes against you beyond a threshold, absolute (-1%), volatility-based, or time-based (after N bars).

Time-based exits: You exit after a fixed holding period, regardless of performance, very useful for simplifying backtests and limiting overfitting.

In ML-driven strategies, you may also consider model-driven exits:

Exit when the model no longer predicts the same direction

Exit when model confidence drops below a certain threshold

Important: the exit must be consistent with your entry logic. If you enter on long-term signals but exit every 3 minutes, your strategy probably won’t make sense.

Also, be careful with overlapping signals, you don’t want your strategy to constantly enter and exit without clear rules (a common cause of slippage and overtrading).

My tip: if someone asked “why did you exit this trade?”, you should be able to answer in one sentence, without hesitation. That’s the kind of clarity you want.

3. Position Sizing: How Much You Trade

Once you’ve defined when to enter and when to exit, the next step is to decide how much to trade on each signal.

This might seem like a detail, but it often makes the difference between a strategy that survives and one that blows up.

There are multiple ways to size your positions:

Fixed size: always trade 1 unit per signal. Simple, but ignores volatility or conviction.

Volatility-adjusted: scale down when volatility is high to keep your risk stable (e.g. based on ATR or standard deviation).

Confidence-based: if your signal comes from a model, increase size when confidence is high, reduce when low.

Risk-based: aim for a fixed % of your capital at risk (e.g. risking 0.5% of your capital per trade with a known stop).

A few key rules I follow:

Avoid overcomplicating position sizing too early. Complexity here often creates fragility.

Always test the impact of sizing decisions separately from signal quality. Good signals can be ruined by bad sizing.

In the beginning, simple ≠ bad. A fixed size might be all you need until you’ve validated your logic.

Position sizing isn’t just a capital allocation problem, it’s part of your risk management.

My tip: start small, test simple sizing logic, and only scale up complexity if it truly adds robustness.

4. Risk Management: Staying Alive

Even with solid entries and exits, no strategy survives without proper risk management. This is what keeps you in the game when things go sideways.

1. Core Controls

Stop-loss: Cut losses fast.

Max drawdown: Pause or reduce if your equity dips too much.

Time stop: Exit after a max holding time, even if no signal.

Daily cap: Limit daily loss to avoid spirals.

2. Multi-Strategy Risk

Running several systems? Check for hidden correlations. Strategies that seem different can fail together. You need risk rules not just per strategy, but for your full portfolio. We will detail that in one of the next newsletter.

3. Failsafe Mode

What if everything breaks?

Reduce size automatically when PnL dives or volatility spikes.

Pause if live results diverge too far from expected.

Risk management isn’t about perfection. It’s about staying alive long enough to keep improving.

👉 If you want to go deeper into each step of the strategy building process, with real-life projects, ready-to-use templates, and 1:1 mentoring, that’s exactly what the Alpha Quant Program is for.

It’s the full roadmap I use to turn ideas into live strategies.