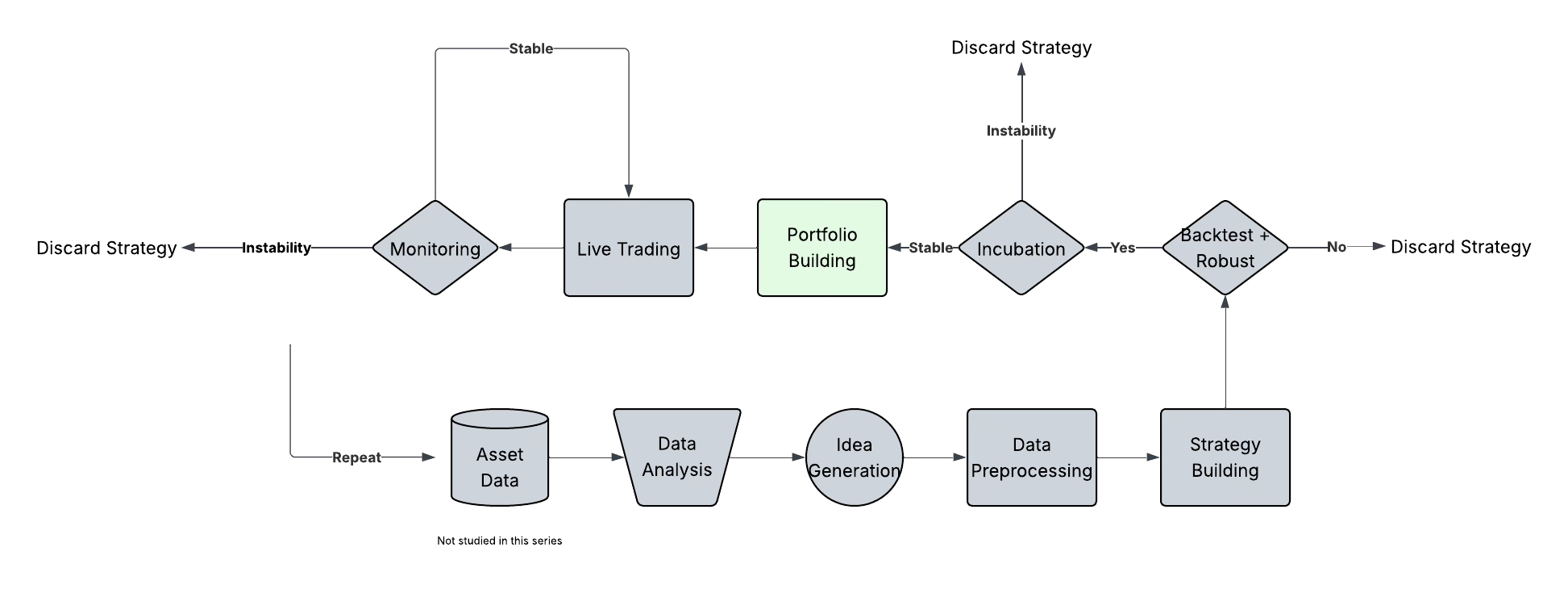

Build the Performance You Actually Want (7/8)

It’s about combining good ones that fail at different times

You’ve built a strategy. You’ve backtested it, incubated it, maybe even traded it live.

It works.

But then the market shifts. Volatility spikes. Your edge fades.

And suddenly, your whole system is on pause.

That’s the limitation of relying on a single strategy, no matter how strong it is, it won’t work all the time.

The solution isn’t to build the perfect strategy.

It’s to build a portfolio of strategies each with different logic, assets, or timeframes, designed to compensate for each other’s weaknesses.

In this newsletter, we’ll explore why this shift from individual strategy to portfolio thinking changes everything.

We’ll look at the obvious benefits, how to tailor your allocations to your own investor profile, and why combining average strategies can often lead to far better results than trying to optimize just one.

👉 If you want to go deeper into each step of the strategy building process, with real-life projects, ready-to-use templates, and 1:1 mentoring, that’s exactly what the Alpha Quant Program is for.

It’s the full roadmap I use to turn ideas into live strategies.

1. The Obvious Benefits

Let’s start with what you can see right away.

Running multiple strategies isn’t just about diversification for its own sake.

It’s about creating something that performs better together than any individual part could on its own.

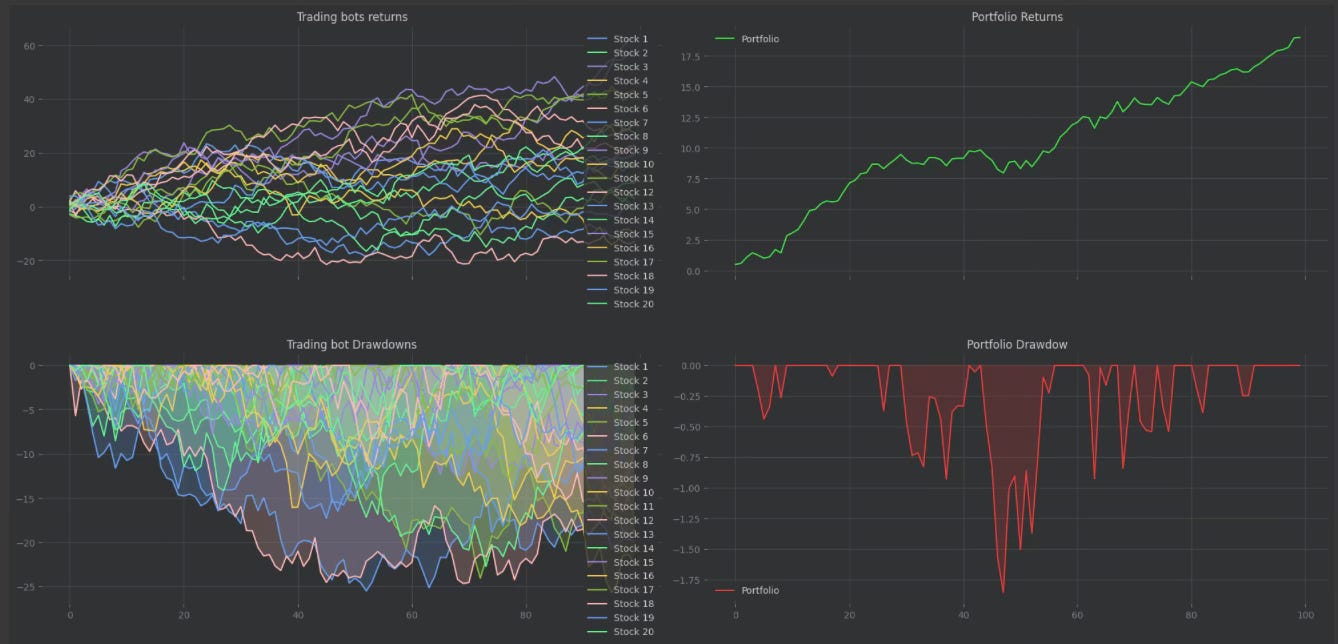

Look at the image below:

On the left, you’ve got 20 trading strategies, each with its own path. Some do well, others struggle. A few go into deep drawdowns.

On their own, you’d have to pick carefully. The wrong one could kill your year.

Now look at the right. That’s what happens when you combine them evenly into a portfolio.

The return curve is smoother

The drawdowns are shallower

The trajectory is more stable, because it’s not dependent on any single strategy being perfect

This is the power of aggregation.

You don’t need to find the best strategy. You need a group of good, uncorrelated ones.

When one underperforms, another can pick up the slack. When volatility rises, different timeframes react differently. When one regime ends, another begins, and with it, a different strategy shines.

You’re no longer betting on a single logic. You’re building a system of systems, and that changes everything.

My tip: If you’re still trying to find the one perfect strategy, stop. A portfolio of imperfect ones, well-balanced, will take you much further.

2. Align With Your Risk Profile

Building a portfolio isn’t just about reducing drawdowns.It’s about designing the kind of performance you actually want.

Some traders chase returns. Others can’t stand volatility. Some want stable monthly income. Others are fine with long periods of flat performance if the long-term payoff is strong.

When you trade multiple strategies, you get to choose your blend.

Want more stability? Allocate more to low-volatility, high-win-rate systems.

Want faster growth? Tilt toward momentum or breakout-based strategies, even if they’re more volatile.

Want to hedge directional exposure? Mix in mean-reverting or neutral strategies.

It’s not just about Sharpe ratio or CAGR anymore.

It’s about fit, between your portfolio and your psychology.

The same 5 strategies can produce very different results depending on how you allocate between them.

And you don’t need a perfect formula to start.

Even a simple approach like equal weights or volatility-scaling can already make a big difference.

The key is: you’re not stuck with what a single strategy gives you.

You now have control over the shape of your returns.

My tip: If your trading results make you uncomfortable, the problem might not be the strategy, it might be the allocation. Design a portfolio you’re actually willing to hold through uncertainty.

3. Volatility Reduction Done Right

Here’s something most traders overlook:

You don’t reduce volatility by smoothing out one strategy.

You reduce it by combining different behaviors.

Look again at the drawdowns from earlier. Each individual strategy experiences sharp drops, sometimes brutal. But when you put them together, those drops rarely happen at the same time.

The result ? A portfolio with lower max drawdown, even if the components are far from perfect.

This is the power of uncorrelated risk. When your strategies react differently to market conditions, their pain points are spread out. One struggles during high volatility? Another thrives. One is dormant in ranges? Another picks up the breakout.

And when the rough periods don’t overlap, your equity curve starts to smooth out.

You don’t just get better stats, you get better survivability.

That’s not a coincidence.

It’s the effect of well-constructed diversification.And no, this doesn’t mean adding random strategies.

It means thinking carefully about logic, timeframes, instruments, and structure.

Because when you do it right,

You don’t just reduce volatility, you build confidence.

My tip: If you want smoother performance, don’t over-optimize one strategy — combine several that fail at different times. Diversification isn’t about quantity. It’s about timing your weaknesses.

A strong portfolio isn’t built once. It’s something you shape, adjust, and refine over time.

Because markets change, strategies decay, and what worked yesterday might not work tomorrow.

That’s why the process doesn’t end here.

In the next newsletter, we’ll talk about why this entire cycle, from idea to execution, needs to repeat.

And how to build a research loop that keeps your edge alive.

👉 If you want to go deeper into each step of the strategy building process, with real-life projects, ready-to-use templates, and 1:1 mentoring, that’s exactly what the Alpha Quant Program is for.

It’s the full roadmap I use to turn ideas into live strategies.