Integrating Exogenous Drivers into Market Models

How global indices like S&P 500, Gold, or Oil can reveal hidden dependencies across assets.

Most quantitative models treat each market as if it were isolated.

In reality, no asset lives in a vacuum. Global indices like the S&P 500, Gold, or Oil capture broad economic forces, growth expectations, inflation, risk appetite, and liquidity, that constantly shape local price dynamics.

When these global drivers shift, they often leave fingerprints across markets.

An FX pair might react to equity volatility, a commodity might follow risk sentiment, and an index might move in sync with credit spreads.

Ignoring these relationships means missing part of the information flow that defines the real market environment.

Integrating exogenous variables is not about adding more data for the sake of it. It is about reconnecting models to the world they operate in, understanding whether global drivers truly influence your universe, and under which conditions that influence becomes dominant.

👉 If you want to go deeper into each step of the strategy building process, with real-life projects, ready-to-use templates, and 1:1 mentoring, that’s exactly what the Alpha Quant Program is for.

1. Identifying Exogenous Drivers

Not all external variables are meaningful. The key is to select a few that capture the main economic dimensions influencing global markets.

Each represents a distinct layer of macro behavior, risk, liquidity, growth, or uncertainty, that can propagate across assets.

Some of the most useful exogenous indicators include:

Equity risk proxies: S&P 500, NASDAQ, MSCI World (risk sentiment and growth expectations)

Commodities: Oil for global demand and inflation pressure, Gold for risk aversion and real rates

Rates and currencies: US 10-year yield, DXY Dollar Index (liquidity and policy dynamics)

Volatility indices: VIX or MOVE (systemic uncertainty and volatility regimes)

By aligning these drivers with your own universe, you can test whether the behavior of your assets follows global trends or remains idiosyncratic.

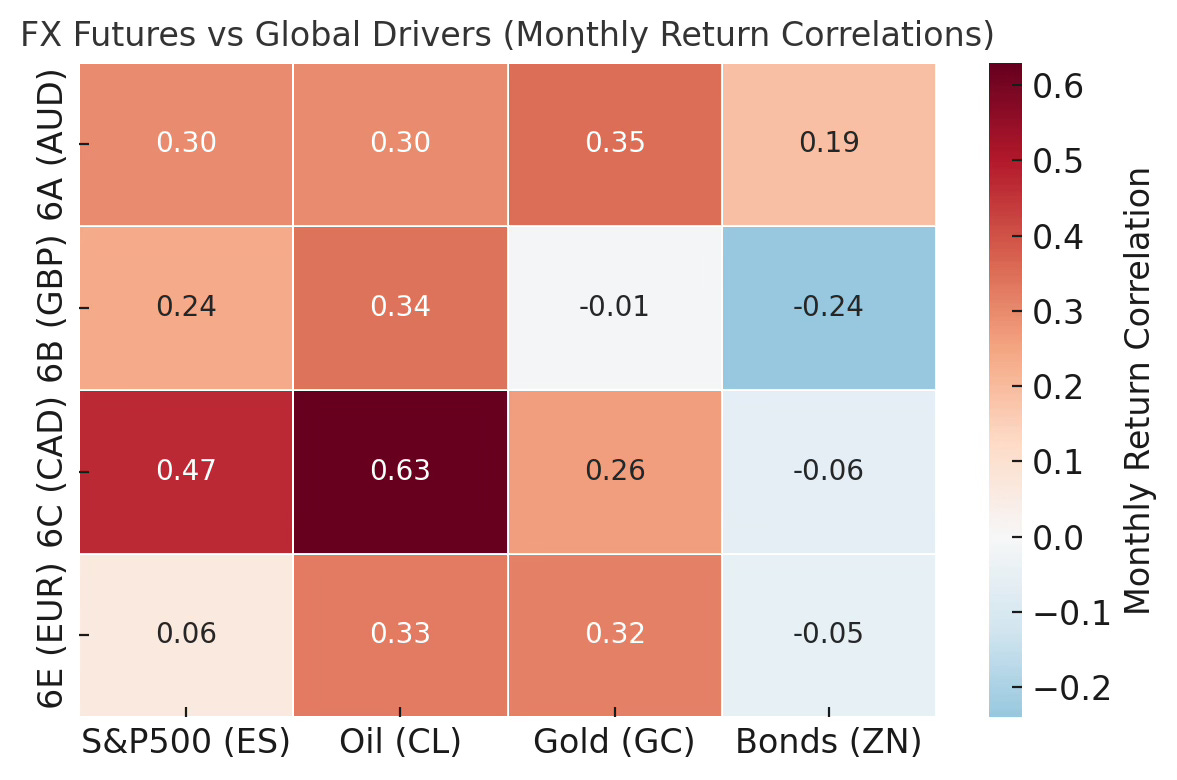

Commodity-linked currencies (AUD, CAD) show strong positive links with Oil and equities, while EUR and GBP remain relatively neutral or weakly connected. Gold and Bonds act as defensive counterweights in most cases.

This first diagnostic step helps you identify what truly matters before moving on to deeper modeling.

2. Measuring the Influence

Understanding correlations between price returns gives a first idea of global connections, but volatility often tells a deeper story.

Instead of measuring how assets move together, we can look at how uncertainty propagates across markets.

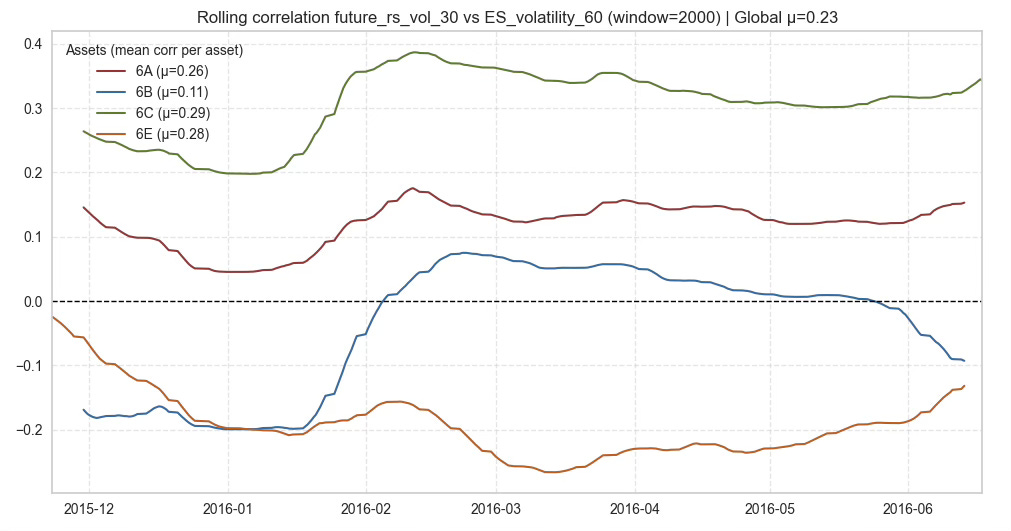

The chart below shows the rolling correlation between the future realized volatility of FX futures (30-period) and the past volatility of the S&P 500 (60-period).

In other words, it tracks how shifts in equity volatility translate into later volatility changes in FX markets.

Volatility shocks in equities often echo into FX markets, especially for commodity-linked currencies like CAD (6C) and AUD (6A). The global average correlation remains around 0.23, confirming that risk flows are transmitted rather than isolated.

This analysis highlights a critical point:

Market volatility is not random. It spreads through channels of liquidity, sentiment, and global positioning.

When equity volatility rises, FX volatility tends to follow, not instantly, but with a measurable delay.

Such insights help identify when macro shocks are likely to affect your universe, and which assets are structurally more exposed to global risk transitions.

Integrating exogenous drivers into market analysis is not about making models more complex.

It is about understanding the global context in which your strategies operate.

By studying how volatility, returns, or features from broad indices like the S&P 500, Oil, or Gold interact with your asset universe, you uncover how information and risk flow through markets.

Some connections remain weak and local; others reveal deep structural dependencies that persist across time.

The analysis of volatility transmission shows that even when assets appear independent, global conditions quietly shape their behavior.

Recognizing these patterns allows you to anticipate when external shocks might alter your model’s environment, and adjust accordingly.

True robustness comes from awareness, not complexity.

The more your models understand the world they live in, the more resilient they become.

👉 If you want to go deeper into each step of the strategy building process, with real-life projects, ready-to-use templates, and 1:1 mentoring, that’s exactly what the Alpha Quant Program is for.