How to Survive the Multiple Hypothesis Bias

Why Most Strategies Fail Before They Even Reach Live Trading

Most quant strategies fail long before they ever reach live trading. Not because the idea is bad, not because the model is weak, but because the research process silently falls into the multiple hypothesis bias. The more features you try, the more targets you test, the more parameters you tweak, the higher the chance that you end up with a strategy that only worked thanks to randomness. On paper it looks clean. In reality it dies instantly.

The real danger is simple. You are not validating an edge. You are validating your ability to overfit a dataset.

This problem does not disappear with stricter statistics. It disappears with a structured process. A process that forces you to observe the data before trying to exploit it. A process that tests ideas across assets instead of squeezing the last bit of Sharpe from one isolated backtest.

This is where research stops being guesswork and starts becoming reliable.

1. The Silent Failure of Quant Strategies

Most strategies do not collapse in live trading. They collapse much earlier, at the research table. The moment you generate dozens of features, try multiple targets, tweak thresholds, change windows, adjust filters, and rerun the backtest until the curve finally looks acceptable, you have already lost. What you found at that point is not an edge but a statistical accident.

The multiple hypothesis bias creates a simple illusion. The more you test, the more likely you are to validate randomness that looks like skill. It feels scientific because the process involves charts, correlations, mutual information scores, or ML validation metrics. In reality, you are only increasing your exposure to luck.

There is no way to beat this bias by looking harder at the same dataset. The only way to survive it is to change how ideas are produced, documented, and validated. A process that forces discipline removes most of the freedom to overfit and brings you closer to discovering signals that survive contact with real markets.

2. The Process First Defense

The multiple hypothesis bias cannot be defeated by adding more statistics. It can only be controlled by reducing the freedom you have to overfit. This is where a structured research pipeline becomes your first line of defense.

Everything starts with the global lifecycle of a strategy.

This sequence matters because it removes the temptation to jump directly from a raw idea to a shiny backtest. Each stage narrows what is allowed and what is not.

• Data Processing ensures clean, aligned, reproducible data.

• Strategy Designing forces you to observe, document, and justify relationships before turning them into signals.

• Backtest and robustness testing validate the logic rather than the curve.

• Incubation confirms that the behavior survives real market conditions without committing capital.

This is how you cut 80 percent of the overfitting before even pressing Run Backtest. You shift the work upstream. Instead of asking whether the strategy performs well, you ask whether the process that created it is capable of producing a stable and repeatable signal.

Once the pipeline is defined, randomness has far fewer places to hide.

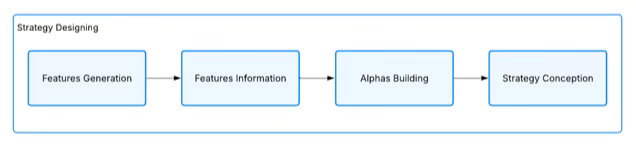

3. Inside the Strategy Designing Block

To eliminate most of the multiple hypothesis bias, you need a clear structure for how ideas are generated, evaluated, and transformed into something tradable. This is the role of the Strategy Designing block.

This block forces you to slow down. Instead of running endless tests, you extract information step by step.

Feature Generation

Create candidate variables without trying to predict anything yet. This stage expands the information you have about price behavior, volatility regimes, order flow, or structural patterns. You are not looking for performance. You are looking for raw material. You can also explore the Quantreo library which provides +35 ready to use free feature templates.

Feature Information (DSR)

Document what is actually observed in the data. Definition, Stability, Robustness (DSR rule). This is where most people fail. They see a correlation and jump straight to a backtest. You do the opposite. You verify whether the pattern is stable through time, consistent across assets, and present outside the window that made it look attractive.

Alpha Building

Turn an observation into a justified signal. A valid alpha is not “this feature correlates with returns”. A valid alpha explains who loses, which bias creates the opportunity, and why the inefficiency persists (LBP rule). This removes the fragility that usually kills statistical edges.

Strategy Conception

Translate the alpha into entry, exit, and sizing rules that can actually be deployed. This step transforms a mathematical intuition into a rule that can be tested fairly and repeated in live trading.

When this structure is respected, the search space shrinks naturally. Fewer random patterns survive. What remains has a higher chance of being real.

4. Robustness Beyond the Backtest

A clean equity curve does not prove that an idea is good. It only proves that the process used to generate this idea was either disciplined or extremely lucky.

Most curves that look impressive are the result of over-optimisation, implicit data leakage, or hidden assumptions that never survive real markets.

Robustness starts before the backtest. You test the logic, not the performance.

One of the most effective ways to reduce the probability of a lucky strategy is to verify whether the same behavior appears across different assets. If your signal only works on one symbol, one timeframe, or one regime, it is probably randomness. When a relationship appears on several markets with different dynamics, the probability that it is real increases sharply.

The same principle applies to market regimes. A pattern that holds in high volatility but disappears in low volatility is not useless, but it must be treated as conditional.

You do not need perfect universality. You need consistency that survives segmentation.

True robustness comes from confronting the idea with environments it was not optimised for. Test it on other assets. Test it on other time windows. Test it on volatility buckets. Test it without the filters that made the backtest look clean.

A backtest is designed to push the strategy to its limits and expose every weakness. Only if it fails to break it do you move to the next stage. The earlier you move robustness checks in the pipeline, the fewer false positives you will carry to live trading.

The multiple hypothesis bias is not a statistical detail. It is the main reason why most strategies collapse before ever reaching live trading. The only way to survive it is to replace guesswork with a structured process. When you generate features in a disciplined way, document relationships with DSR, justify alphas with clear economic logic, and test behaviour across assets and regimes, you remove most of the freedom to overfit.

This is exactly what the AI Trading Lab was built for. It conceptualizes the entire Strategy Designing block and turns it into a guided, AI powered workflow. The agents help you generate better features, extract cleaner information, build justified alphas, and document every step automatically. You focus on the reasoning. The system takes care of the structure.

If you want to build strategies that survive reality instead of strategies that look good on paper, this is where you start.