Cross-Asset Learning: Finding True Structure Beyond Noise

When the same features drive predictability across multiple markets, robustness stops being an accident.

After developing a directional prediction model on a single asset, the next logical question was simple: does it generalize?

In quantitative research, true robustness is revealed when a model performs consistently across different markets, not just on the one it was trained on. If a relationship is structural rather than random, it should reappear independently in other datasets.

This study explores that idea by testing the same directional XGBoost model across four FX futures, 6A, 6B, 6C, and 6E. Each model was trained separately, using non-linear market features such as slope, volatility, tail asymmetry, and cross-scale alignment.

The goal was to see whether the same relationships would emerge again, and whether combining them could lead to a more stable and reliable predictive signal.

👉 If you want to go deeper, build smarter features, understand signal reliability, and master techniques like features selection, features engineering, or feature conditioning, that’s exactly what we cover in ML4Trading.

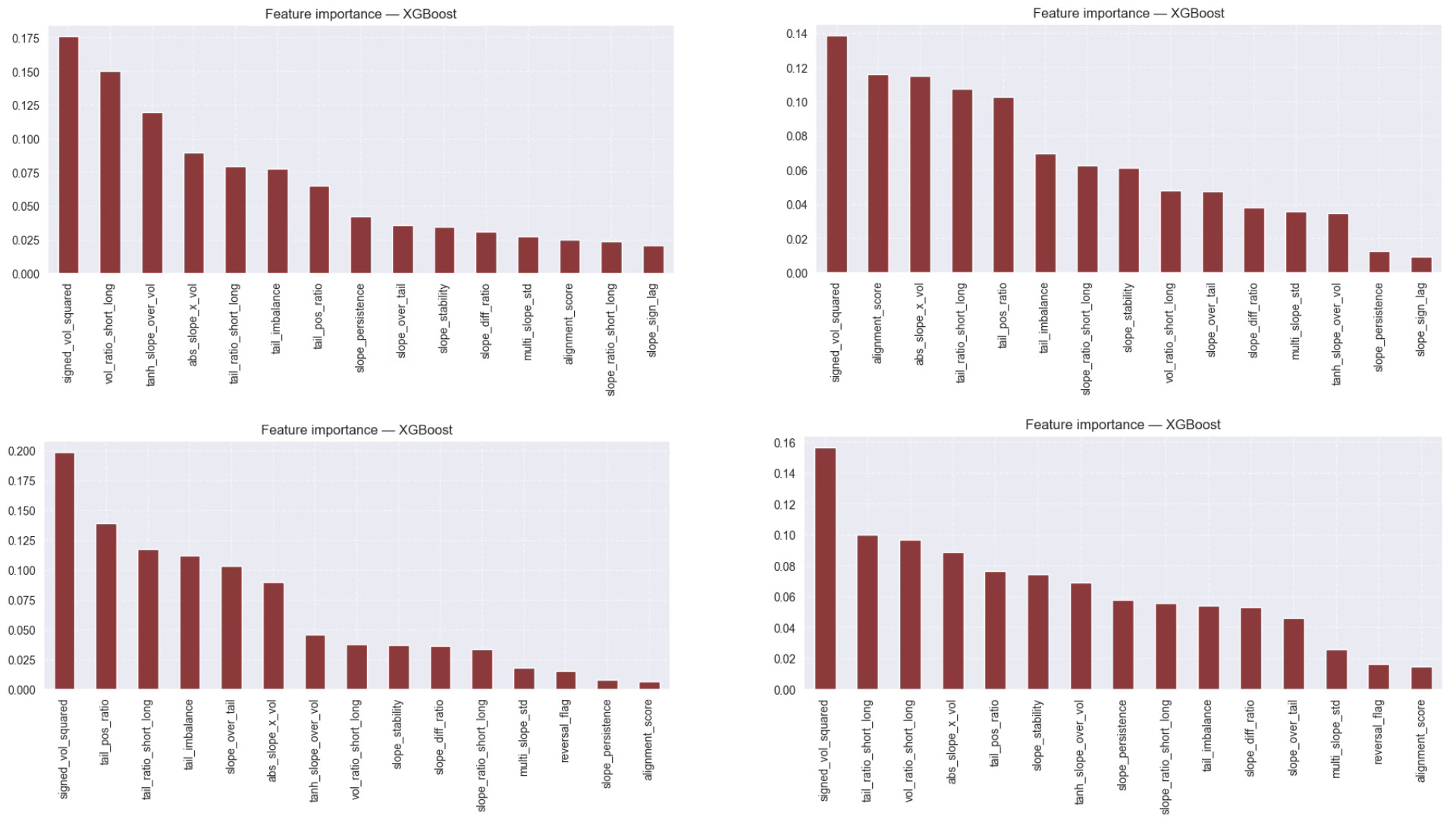

1. Feature Stability Across Assets

Each market was modeled independently, yet the results tell a remarkably consistent story.

Across all four FX futures, the same group of features keeps emerging at the top of the XGBoost rankings: signed_vol_squared, vol_ratio_short_long, and tail_ratio_short_long.

These variables combine information about volatility intensity, relative volatility across scales, and directional asymmetry in returns. Their recurrence across assets suggests that the model is not learning noise, but capturing a genuine structural mechanism that links volatility patterns with directional bias.

This kind of cross-asset consistency is rare. It provides strong evidence that the signal is not accidental or overfitted, but rooted in market behavior itself.

The same features dominate across all markets, confirming structural robustness.

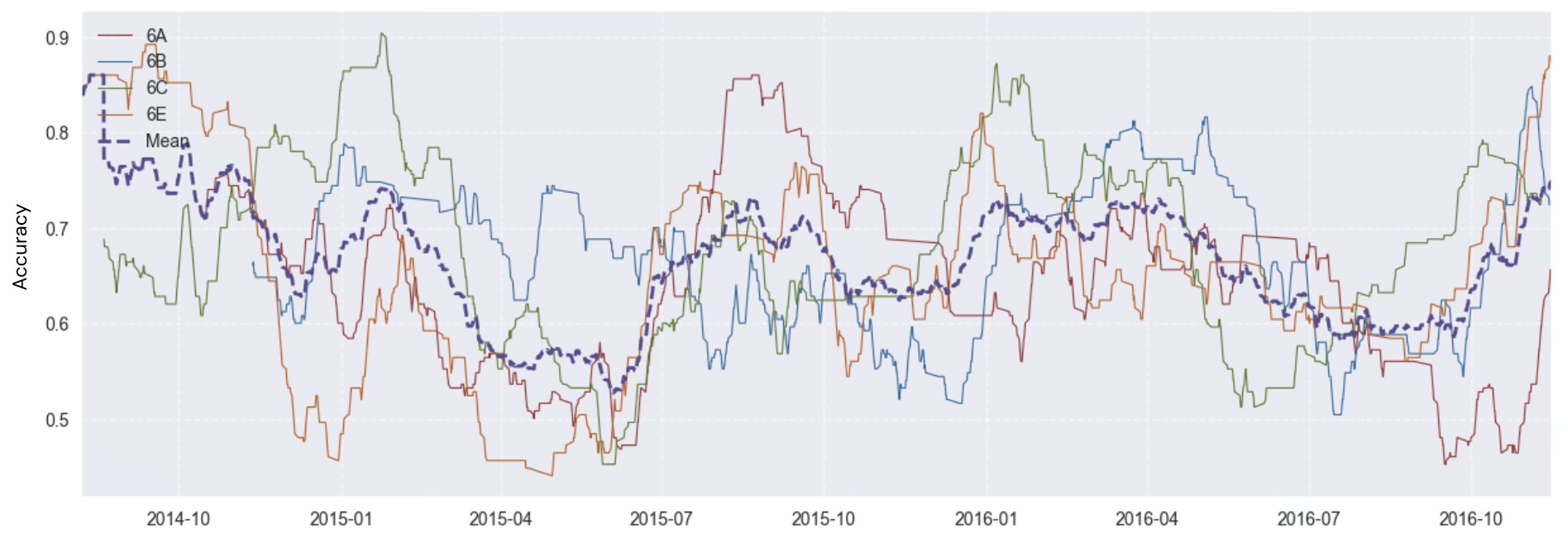

2. Rolling Directional Accuracy

While feature importance reveals structural consistency, performance over time tells another part of the story.

Each model reaches periods of higher or lower accuracy depending on market regime, volatility, and liquidity conditions.

Yet when we look at them together, a clear pattern appears.

The chart below shows the rolling directional accuracy (250-point window) for all four FX futures.

Individually, accuracy fluctuates between 0.55 and 0.75, but the ensemble mean, shown as the dashed line, remains steady around 0.65.

The combined signal is smoother and more reliable than any single model.

This result demonstrates that robustness can come from diversity.

Each asset reacts differently to changing market regimes, so their errors are only weakly correlated.

When averaged, these independent variations cancel out part of the noise, revealing a more stable and persistent edge.

3. Interpretation

Two forms of robustness emerge from this experiment.

First, structural robustness, shown by the repeated dominance of the same features across all markets.

Second, temporal robustness, visible in the smoother ensemble signal built from multiple independent models.

Together, they suggest that the model captures a real, repeatable mechanism linking volatility dynamics, directional persistence, and tail asymmetry.

Even though each asset experiences different shocks and liquidity cycles, the underlying relationships remain stable.

This reinforces an important principle in quantitative modeling:

a signal that survives across assets and timeframes is far more valuable than one that only works perfectly in isolation.

This cross-asset experiment confirms that robustness is not an accident but a property that emerges when structure repeats itself across different markets.

When the same features drive predictability in four independent assets and when their signals combine into a smoother and more stable output, the conclusion is clear: the model is learning something real.

Averaging across assets transforms small, inconsistent edges into a durable and interpretable signal.

Instead of optimizing a single market, we let diversity reveal structure, and structure, in turn, creates stability.

In practice, true robustness comes from replication, not perfection.

👉 If you want to go deeper, build smarter features, understand signal reliability, and master techniques like features selection, features engineering, or feature conditioning, that’s exactly what we cover in ML4Trading.

Thank you very much Lucas.

I was wondering what would be the practical use of the ensemble mean of rolling directional accuracy. How would you use it in to improve a model?