Adapting Strategies to Market Structure

Understanding when (and where) your strategy truly performs.

Markets do not behave the same way all the time. Their structure shifts with the hour, the day, and the trading session.

Liquidity, volatility, and participation are not constant, and these patterns quietly shape how every strategy performs.

A trading model that works perfectly during London hours might fail in Asia, not because the logic is wrong, but because the market environment has changed.

Volume, volatility, and order flow structure define the context in which a signal can express itself.

Understanding these structural behaviors is the foundation of adaptive trading.

Instead of asking “does my strategy work,” the better question is “when does it work best.”

👉 If you want to go deeper into each step of the strategy building process, with real-life projects, ready-to-use templates, and 1:1 mentoring, that’s exactly what the Alpha Quant Program is for.

1. Structural Patterns

Every market has its rhythm. Activity and volatility expand and contract depending on where global liquidity is concentrated.

By studying recurring structural patterns, we can identify when conditions are most favorable for execution or signal reliability.

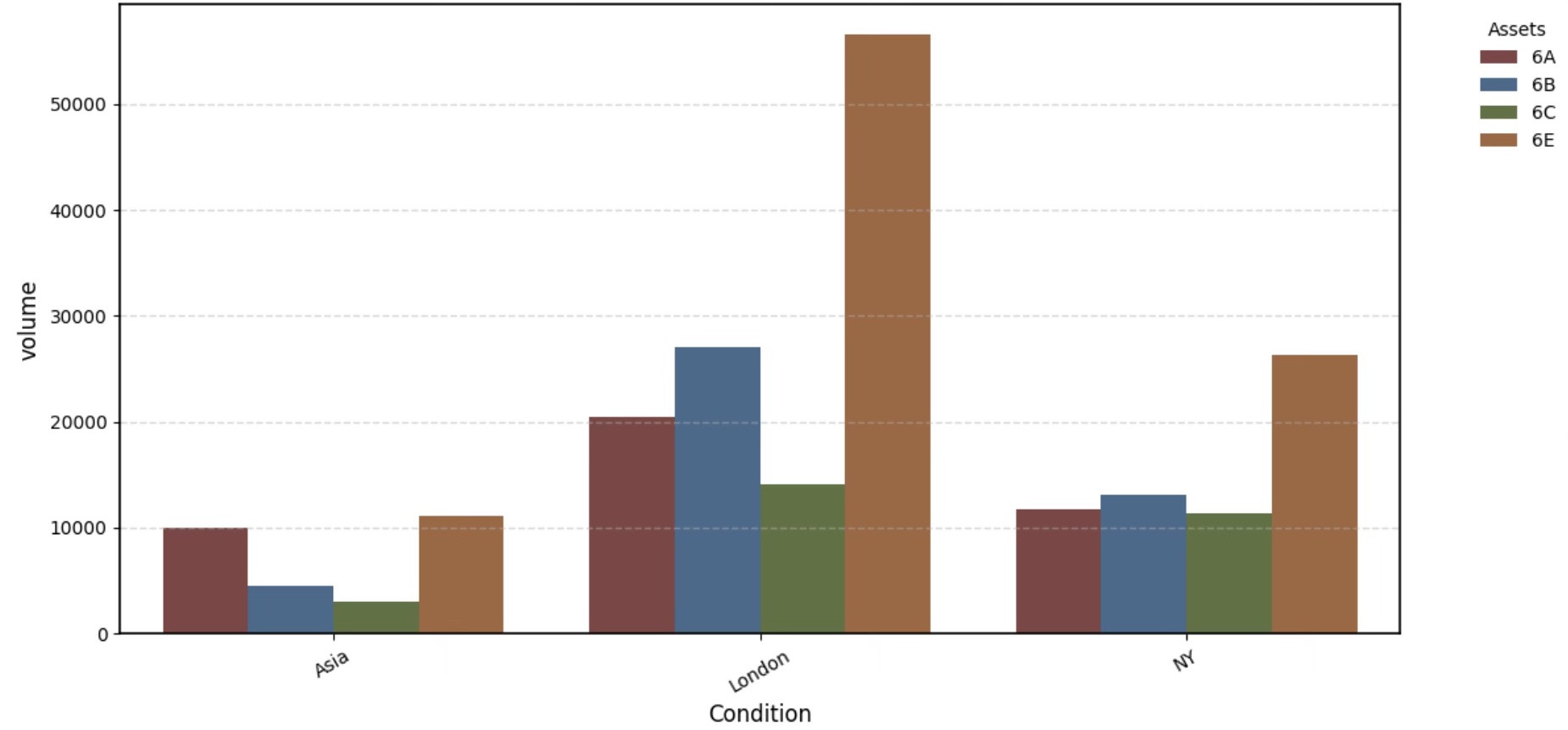

The chart below shows the median trading volume across the three main sessions: Asia, London, and New York.

London dominates activity, while Asia shows lighter and more stable conditions.

This simple observation already tells a story.

A strategy that depends on liquidity and tight spreads should operate mainly during the London or New York sessions.

Conversely, a strategy sensitive to noise or volatility spikes might perform better in the calmer Asian hours.

Such structural insights are not cosmetic details. They define when the market provides the right environment for your strategy to function as designed.

2. From Observation to Adaptation

Identifying structural patterns is only the first step. The real value comes from linking them to performance metrics such as P&L, hit ratio, or drawdown stability. When you group your backtest results by regime, session, day of the week, or volatility state, you start to see where your strategy truly belongs.

For example:

A momentum or breakout model may show its best behavior when volume and volatility are both high.

A mean reversion setup may perform better when the market is quiet and spreads are wide.

Execution models can be tuned to run only in London or New York, where depth and participation are sufficient.

This type of contextual analysis turns a static strategy into an adaptive one.

You no longer judge your edge globally, but within the specific market environments that support it.

PS: this type of analysis should be done on a small, separate sample of data. Doing it on the full dataset and then selecting the best condition would introduce a strong bias and overstate robustness.

Robustness is not only about surviving every market condition. It is about knowing when your strategy performs at its natural best.

By analyzing structural behavior, volume, volatility, and session patterns, you move from static validation to contextual intelligence.

A strategy that understands its environment becomes more reliable, easier to monitor, and easier to scale.

Instead of forcing performance everywhere, you let the market tell you where and when it wants to cooperate.

The edge is not just in the model, but in the conditions that let it breathe.

👉 If you want to go deeper into each step of the strategy building process, with real-life projects, ready-to-use templates, and 1:1 mentoring, that’s exactly what the Alpha Quant Program is for.